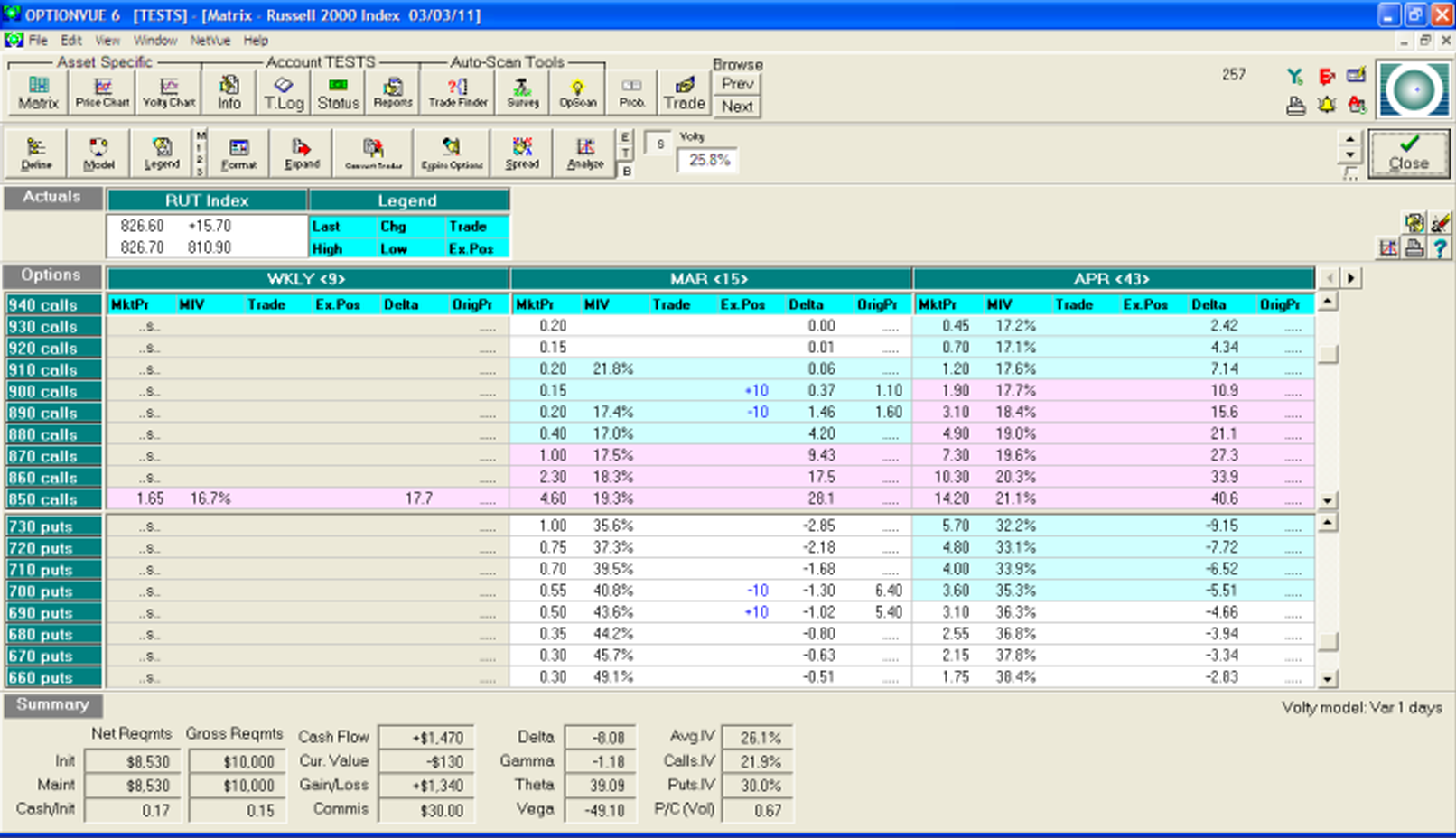

One of the most popular income options strategy is known as the high probability iron condor, which consists of a call side credit spread and a put side credit spread “facing each other” very far out of the money. For example, on January 19, 2011, at about 10:30 in the morning, the RUT Index was trading at 798. An options trader could have sold a ten lot March 700-690 put credit spread for 1.00 (selling the 700 puts for 6.40 and buying the 690 puts for 5.40) and simultaneously sold a March 890-900 call credit spread for .50 (selling the 890 calls for 1.60 and buying the 900 calls for 1.10). Excluding commissions, the total spread would have yielded a credit of 1.50 times 1000 options contracts, or a total credit of $1,500 less commissions and exchange fees.

Theoretically, if the RUT index opens between 700 and 890 on the Friday of March expiration week, the trader would pocket $1,500, less commissions and exchange fees. On the other, the worst case scenario of this trade is for the trader to pull a Rip Van Winkle, fall asleep for the 59 days it would take for all of these options to expire and find that the RUT index had opened below 690 or above 900 on the Friday of March expiration week. In that case the trader would lose $10,000 less the original $1,500 credit that was received, for a net loss of $8,500.

As options expirations day approaches, invariably the credit spread on one side of a condor or the other, or in very favorable months both sides, will shrink to 10% or less of its original value. That is because the short option on one or both sides of the trade is so far from the money with so little time left that the market demand for that short has almost evaporated, dropping the value of that short option and the long protecting it to nearly nothing.

Let’s look at that same condor today. As of this writing, both the call side and the put side credit spreads have shrunk to 5 cents in value each, or $100 in total. In other words, the entire condor, for which we received $1,500 could be covered for a cost of $100, netting us a $1,400 gain less commissions and exchange fees.

During my early years of trading options for income, whenever any of my fellow options trainees found themselves in such a situation, my first options mentor and good friend, Dan Sheridan, would question why we were still in the trade as opposed to doing the sensible thing, which would be to close the credit spreads and apply our capital to other trades with appropriate risk-reward trade-offs. I remember one occasion on which my long time trading partner and close friend Anthony was challenged by Dan in just such a situation. He conjured up the following image: “Anthony, just pretend that you had to go in front of the Anthony Corporation Board of Directors and explain why you were still in this condor, when your only remaining upside is $100 while your downside is $8,500. What do you think they’d say?”

There comes a point in each income options trade when the REMAINING potential upside is so minimal that staying in the trade is foolish. Whenever you are in that situation, close your eyes, picture yourself stammering in front of your own personal board of directors, then open your eyes, put the order in for a dime to close the condor, and move on to your next ” good trade”.

4 Comments on “The Anthony Corporation Board of Directors”

Seth, I really enjoy your options blog! Thanks for sharing your experience…I work full time and trade options on the side, so I have been learning for three years…in your experience, what is the most common way to adjust one leg of an iron condor that may go ITM…my initial thought is to simply place a stop order to close the position. What do you prefer to do with a leg that may go ITM?

Robert,

That’s a difficult question to answer without knowing the particulars of the condors that you sell. The shorts of the high probability iron condor I described in the blog post would never be allowed to be remotely close to in-the-money.That would be catastrophic in fact. Other condor approaches might involve shorts so close to each other that an adjustment could occur at or even past the short strike. One of the most common adjustment techniques is to roll the threatened short strikes farther out of the money, but there are many considerations that are too numerous to discuss in this reply. We will be covering this issue at length in the course when we launch it. Take care.

Yes, absolutely good advice. However, it takes quite a long time, even close to expiration, to have an upside remaining profit of $100 (already pocketed $1400), while the dollar risk remains at $8500. (Gamma risk being the real killer) So if you’re still holding for the last $100 more than likely you have no business putting on a iron condor yet, or you’re just stupidly greedy. Either way the market will eventually take all your money. Take a chunk of what the option gods give you, be happy with it and move on to the next winner:)

YAY RISKREWARD

YAYYYYYYYYYYYYYYYY WHARTON